Following the Government’s release of the Board of Taxation’s report on tax arrangements applying to collective investment vehicles in 2015, the Government has today released an exposure draft of legislation for the new corporate collective investment vehicle.

The new form of corporate collective investment vehicles, to be known as CCIVs, will more closely reflect the form of fund vehicles used in a number of jurisdictions internationally and have been created in an attempt to provide a more efficient form of fund vehicle for fund managers, while at the same time as providing enhanced consumer protections.

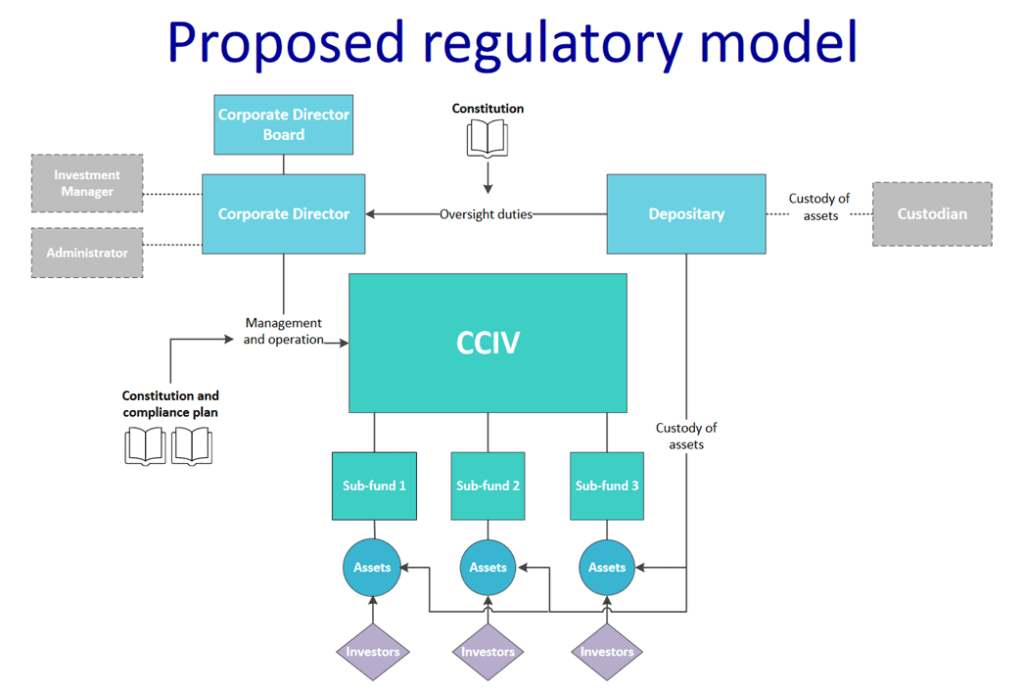

The proposed key features of the CCIV will be:

- CCIVs will be regulated and administered by ASIC

- CCIVs can be open ended or closed ended

- CCIVs will be a separate legal entity and must have at least one sub-fund

- Sub-funds will not have a separate legal identity however if there are multiple sub-funds, the assets of each will be segregated and insolvency remote

- CCIVs may be wholesale or retail

- CCIVs must have a single corporate director:

- The corporate director will be required to have a majority external board

- The corporate director will be entitled to, but not obliged, to delegate functions

- Like a responsible entity of a registered managed investment scheme, the corporate director:

- Must be a public company

- Must hold an appropriate AFSL

- Must ensure compliance with the law and the CCIV’s constitution

- Owes duties to the members (including a best interests duty)

- Will be liable to the members for breach of duty

- Can appoint a manager and/or administrator

- Unlike a registered managed investment scheme, a retail CCIV must have an independent depository which will hold custody of the CCIV’s assets and have oversight functions

- The depository of a retail CCIV will be entitled to delegate custody of CCIV assets but will not be entitled to delegate its oversight functions

- The depository must assume liability for loss of assets held on trust and loss resulting from breach of duty

- The CCIV will have a constitution, compliance plan and compliance plan auditor, but will not have a compliance committee (as a result of the requirement that the corporate director have a majority external board)

- The CCIV will be tax transparent, similarly to registered managed investment schemes

- Registration will be similar to registering a registered managed investment scheme. Each CCIV will have an ACN and each sub-fund will have an Australian Registered Fund Number

- A CCIV must notify ASIC of each sub-fund and its investment strategy before offering shares which carry an interest in a new sub-fund

- CCIVs must notify ASIC of any subsequent material changes to the information provided to ASIC as part of its registration

- Rules governing meetings will be in line with those apply to registered schemes, rather than the rules for bodies corporate

Whilst the exposure draft legislation does not deal with taxation issues, the explanatory materials accompanying the exposure draft reiterate that it is the intention that CCIVs will be tax-neutral in a manner equivalent to Managed Investment Trusts. Like Attribution Managed Investment Trusts (AMITs), CCIVs will be permitted to attribute amounts to specific investors for tax purposes. Similar to the position for AMITs, non-resident investors will typically be taxed at concessional rates on attributable income and will be subject to withholding. Separate exposure draft legislation dealing with tax regime for CCIVs is to be released at a later date.

The Government has asked for submissions on the draft from interested parties. Further details can be obtained here